SaaS is dead and the Agentic Shift

Decoding the Agentic Era

In recent days, SaaS companies have been going lower in worries about the end of the software era or seeing the step change to transforming into the agentic era, and investors are trying to figure it out and looking for answers.

One of my dear friends ShipOfFoolsGD poked me, which helped me to look into it on a deeper level. I took some time to look into it and would like to share it with you all.

Is SaaS really dying?

The short answer is SaaS is not actually dying, and it’s not going away either. No company will switch from digital trackable, verifiable, secure record storage to paper records. At least I haven’t seen it yet. The underlying meaning is that it’s hard to justify the high multiples of software companies. Or will the current SaaS companies maintain their lead in the next step-up change in the agentic era? That’s a better way to phrase the worry investors have.

The SaaS map is changing and evolving. I would say it’s not dying, but it’s filtering out. Some SaaS companies are actually coming out as winners, and some are falling out or at risk of disruption. If the SaaS companies love their high 70-90% gross margin business and are reluctant to accept lower agentic gross margins, they will be in a difficult position and may be ready for disruption. For the agentic era, existing companies don’t necessarily have to be AI native or agentic first. They simply need to adapt it and deploy it for their customers.

As we are going through a major shift, I believe there will be new companies that will emerge, and there will be some existing companies that will become IBM, Cisco, McAfee, and Yahoo of 2000

SaaS is filtering out:

The whole reason I am saying the SaaS is filtering out is that some SaaS companies are becoming essential and even more important in the agentic era. Let’s understand by example.

So far, there are 4 prominent models that are forefront: Opus from Anthropic, GPT from OpenAI, Grok from xAI, and Gemini from Google. The model landscape is changing really fast; it may look different next year. Only time will tell. There is a chance that some industry-specific model emerges as well. For now, these four models are at the forefront. I will keep Google and xAI on the side for now, since they have strong parent companies backing them. Anthropic and OpenAI are emerging AI-native and AI-first companies. Since they are private companies, very little financial information is available, and that’s also not verified by an external entity.

Let’s take a look at Anthropic first. The company that is helping write the code is using quite a lot of SaaS companies in its product technology stack and operations. Just to name a few: CrowdStrike for securing agents, MCP servers, and other AI systems; Datadog for observability; Cloudflare for traffic routing (CDN); Stripe for billing; Greenhouse for recruiting. You can see that in the image below.

I am just sharing here a verifiable SaaS companies list that Anthropic is using; there may be a chance they may use more than this. The interesting thing that drew my attention is that security is non-negotiable in the agentic era. We can verify it by the LinkedIn post, which was posted by CrowdStrike, and more details were published in the blog on the company’s website. You can check here.

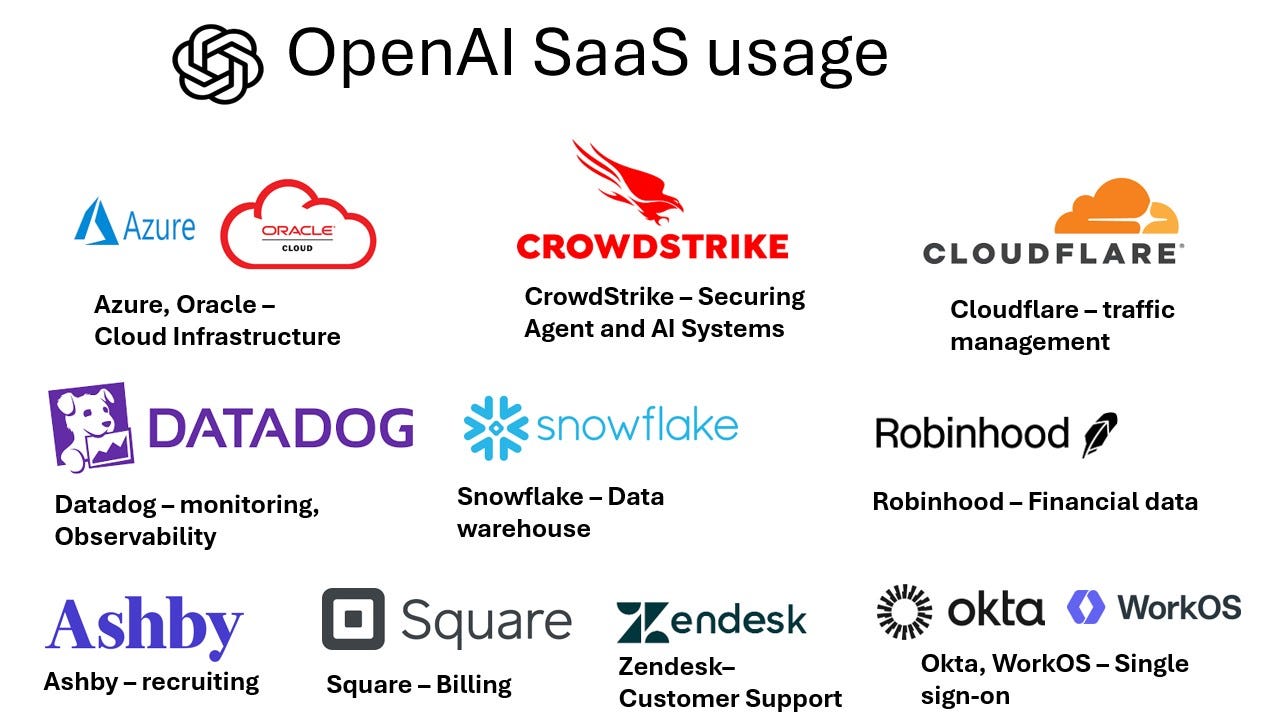

Let’s look at OpenAI. The company is building models for generating images, videos, code, and also for general knowledge. I see a similar pattern to Anthropic; OpenAI is also using other SaaS companies in its product technology stack and operations. Just to name a few: CrowdStrike for securing agents, and other AI systems; Datadog for observability; Cloudflare for traffic management; Snowflake for Data warehouse, Square for billing. You can see that in the image below.

Another similar announcement from CrowdStrike in the press release, OpenAI is designed to add visibility and governance for AI agents that are redefining how work gets done. CrowdStrike Falcon Shield now discovers GPTs and Codex agents created in OpenAI’s ChatGPT Enterprise, expanding support for more than 175 SaaS applications. Read the details here.

The next generation of AI-native and AI-first companies relies heavily on existing SaaS companies. This reliance is why SaaS companies are not dying; instead, they are filtering out the winners in the industry who continue to win. While emerging companies may eventually expand their offerings and build a few solutions in-house, the notion that they will completely abandon SaaS products is a false expectation. It’s beneficial for these companies to focus on what matters most to them rather than divert their attention to building less crucial components in their stack. The competition is intense, and maintaining market share and a competitive edge against juggernauts is no easy task.

Next Generation AI software companies will create massive value:

Let’s look back a bit in history. Hyperscalers (AWS, Google Cloud, Microsoft Azure) have been spending money on data centers since 2010. Unfortunately, all my data points end in 2015, and I don’t have data before 2015. From 2015 to 2023, the data center CapEx totaled between $10 to $15 billion annually for each hyperscaler company. Let’s take the midpoint of $12 billion capex per year per company.

12.5 X 3 = $37.5 billion per year combined 3 companies

37.5 X 9 years = $337.5 billion for 9 years combined by 3 companies.

To put it in perspective, the combined hyperscaler data center capex for the year 2025 was above $325 billion. They allocated capex in a single year that they had combined over the last 9 years. Massive...

Now excluding mag7, the top 40 US software companies added up approximately $2.5 to $3 trillion in market capitalization gains from 2010 to 2025. If you include the broader long tail of hundreds of smaller public software companies, plus the value of companies taken private, the total is likely in the range of $3 to $3.5 trillion. That is almost 10x value creation compared to data center CapEx.

Excluding Mag 7, US software companies generated approximately: $2.5 to $3.0 trillion in cumulative revenue

2016–2020: approximately $750–850B cumulative

2021–2025: approximately $1.2–1.5T cumulative

Software companies in the US have created 10x value compared to the data center CapEx till 2023.

Current AI capex is massive and future CapEx data center is growing like a weed. The increase in numbers is jaw-dropping. In terms of transparency, nobody knows what the real CapEx numbers will be by 2030; it’s all estimates. Let’s take the estimate in the calculation: the current estimate for AI data center CapEx is in the $1 to $2 trillion range. Let’s take a midpoint of $1.5 trillion.

My estimate is that next-generation AI software companies will create at least 5X the value of AI data center CapEx. This is extremely conservative. If we take the AI data center CapEx of $1.5 trillion, then AI software companies will create $7.5 trillion value.

All these will not happen in one year, this is a long term cycle and we are still in early innings.

What will the Agentic era look like?

There will be starter kits and frameworks available for building agents, and every enterprise company will develop its own agents. Browsers and mobile apps will continue to serve as key entry points and major distribution channels for traffic. Additionally, we can expect significantly higher integration and communication among platforms and applications. Something we haven't seen before.

I suggest to focus on identifying who will provide solutions to secure these agents and agentic flows, as well as offer end-to-end observability for agents. Who provides necessary networking and compute to host agents. I think those companies will be keep winning in the agentic era.